If you're hiring a window cleaner right now, you're probably comparing price, availability, and whether the company can handle your property. That's normal. But there's another question that matters just as much: what happens if something goes wrong on your property while the work is being done?

A ladder can shift on decorative stone. A hose can cross a walkway near a storefront entrance. A tool can slip from a technician's hand near parked cars, outdoor furniture, signage, or entry glass. In Phoenix, Scottsdale, Paradise Valley, Chandler, Tempe, and Gilbert, many homes and commercial properties have expensive finishes, high-traffic entrances, and large glass surfaces. The risk isn't hypothetical. It's part of the job.

That's why window cleaning insurance matters. It's not just a business expense for the contractor. It's a layer of protection for the client who invited that contractor onto the property.

Why Window Cleaning Insurance Is Your First Line of Defense

A homeowner in Paradise Valley hires a low-cost cleaner for exterior glass. The crew arrives in an unmarked vehicle, unloads ladders, and gets to work. Midway through the job, a ladder foot slips on a hard surface and scrapes stucco near a picture window. Suddenly, the conversation isn't about spotless glass. It's about repairs, responsibility, and whether the company is able to pay for the damage.

A commercial version is even more serious. A technician working above a retail entrance drops a tool near a busy walkway. No one wants to find out after an incident that the vendor they hired has no active liability coverage, no workers' compensation, and no real process for handling claims.

Practical rule: When you hire a window cleaner, you're not just buying a clean result. You're accepting the risk profile of the company that steps onto your property.

That's where informed vendor selection matters. Property managers already know that preventable contractor issues can become management issues fast. If you work in an HOA or multifamily setting, these tips to avoid HOA mismanagement offer a useful reminder that weak vendor controls often turn into resident complaints, disputes, and unnecessary liability.

Insurance changes the entire conversation. It means there's a formal mechanism to respond if third-party property damage or bodily injury happens during the work. It also signals that the company operates like a real business, not a casual side job with ladders and a bucket.

Clients often focus on the visible part of professionalism: clean uniforms, organized scheduling, purified water systems, and streak-free results. Those things matter. But the less visible part matters just as much. Proper insurance is what separates a polished-looking vendor from a protected, accountable operation.

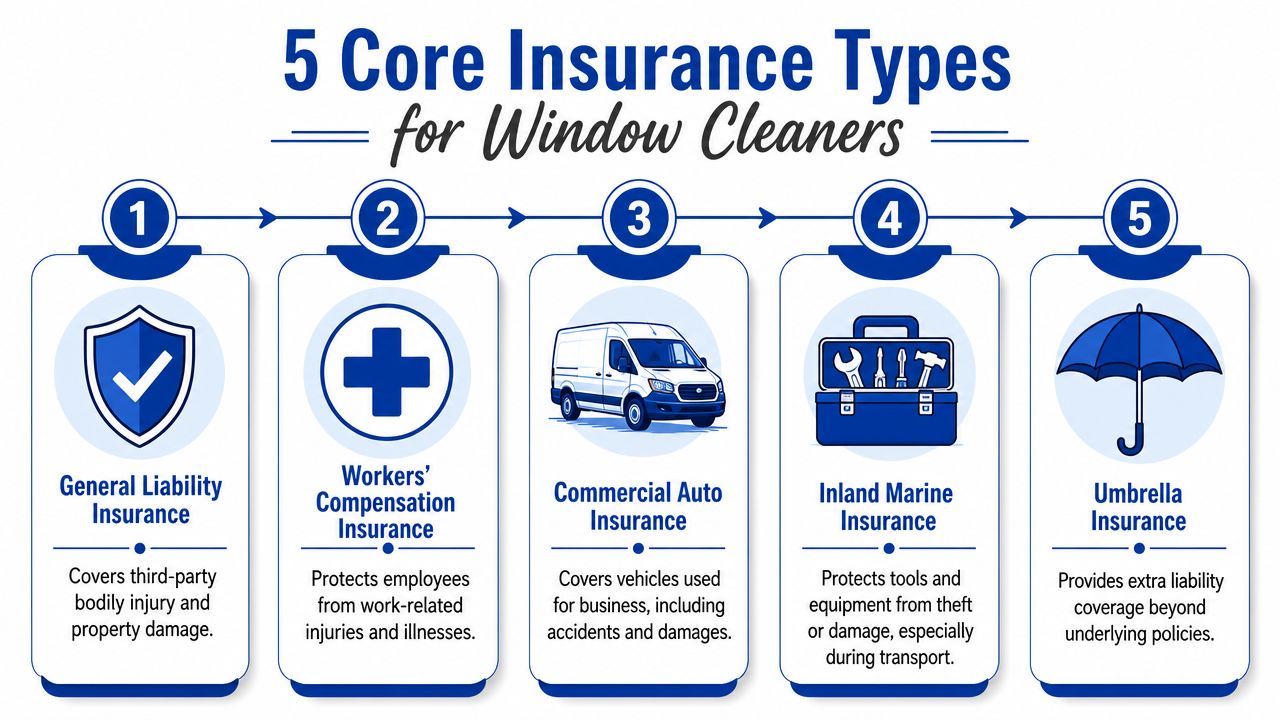

The 5 Core Insurance Types Every Professional Window Cleaner Needs

A crew can look polished and still leave you exposed.

The safer question for a homeowner or property manager is more specific: what kinds of insurance does this company carry, and do those policies match the risks of the work being done at my property? Window cleaning is not a single-risk service. It involves people, vehicles, tools, glass, access equipment, and work performed above walkways, landscaping, finishes, and personal property. One policy rarely addresses all of that.

Here's the visual overview first.

General liability is the policy clients ask for first

General liability usually sits at the center of a professional window cleaning insurance program. It is the policy that commonly responds when the company causes third-party property damage or third-party bodily injury during the job.

For a client, this is the easiest way to frame it. If a technician cracks a light fixture, scratches a surface, damages landscaping equipment, or a passerby is injured by job activity, general liability is often the first policy reviewed.

That matters because a certificate that shows active general liability tells you there is a formal claims mechanism behind the company. If you want a plain-English refresher on policy language before reviewing a vendor's paperwork, this guide on how to read insurance policy is a useful starting point.

Workers' compensation protects the crew and reduces your exposure

Clients often focus on damage to the building and forget the person doing the work.

That is a mistake, especially in window cleaning. Ladder use, roof access, heat, repetitive motion, and lift work all increase the chance of employee injury. NIP Group explains that window cleaning insurance programs commonly include workers' compensation and that pricing in this trade is affected by factors such as height of work, payroll, and claims history, as outlined in their summary of window cleaning insurance types.

From the client side, the point is simple. If someone gets hurt on your property, you want that injury handled through the employer's insurance system, not through confusion, delays, or an uninsured contractor trying to solve a serious problem with personal funds.

Commercial auto covers the vehicles that support the job

A window cleaning company does not arrive empty-handed. It shows up with vans or trucks carrying ladders, poles, hoses, tanks, screens, tools, and chemical supplies.

Commercial auto insurance applies to vehicles used for business and can also matter if an accident happens while the crew is traveling between jobs or maneuvering on site. For property managers, this is one of the most overlooked parts of vendor screening. The vehicle unloading in your parking area is part of the operation, and it carries risk of its own.

Inland marine covers mobile equipment

The name sounds outdated, but the function is practical.

Inland marine insurance usually covers tools and equipment while they are being transported or used away from the company's main location. For a window cleaning business, that can include water-fed poles, ladders, extension tools, pumps, hoses, and other jobsite gear.

Why should a client care about a contractor's equipment coverage? Because uninsured equipment losses can disrupt service fast. A company that cannot replace stolen or damaged tools may miss appointments, improvise with the wrong gear, or cut corners to stay on schedule. Equipment coverage helps a serious operation recover and keep service standards stable.

Umbrella liability adds extra limit above the primary policies

Umbrella liability works like a second tier above certain underlying policies, such as general liability or commercial auto, after those base limits are used up by a covered claim.

This becomes more relevant as property values, traffic, and potential claim severity rise. A small single-story home and a busy mixed-use property do not carry the same exposure. High-end glass, dense pedestrian areas, and multi-vehicle operations can all increase the financial stakes of one incident.

What informed clients should look for

A true professional operation usually carries several policies because each one addresses a different part of the operational risk.

- General liability: Covers third-party bodily injury and property damage tied to the work.

- Workers' compensation: Covers employee injuries that occur in the course of the job.

- Commercial auto: Covers business vehicles and related liability.

- Inland marine: Covers mobile tools and equipment.

- Umbrella liability: Adds extra liability protection above certain primary policies.

The key takeaway is not that every client needs to become an insurance expert. It is that you should know what to ask for and what each policy is supposed to do. Clean windows are the visible result. Proper insurance is part of the operating system behind that result, and it is one of the clearest signs that you are hiring a company built to handle risk responsibly.

Decoding Policy Limits What $1M/$2M Really Means

A property manager approves a window cleaning vendor, sees “$1,000,000 / $2,000,000” on the certificate, and assumes the building is well protected. Then a worker's ladder strikes a glass entry system, a guest is injured during the commotion, and the next question is no longer whether the company is insured. It is how far that policy goes.

That is why policy limits matter. The two numbers look simple, but they answer two different risk questions.

Per occurrence means one claim has one ceiling

The per occurrence limit is the maximum the policy will pay for a single covered incident.

If a window cleaner carries $1 million per occurrence, the policy can respond up to that amount for one event, subject to the policy terms and exclusions. For a client, the practical question is straightforward. If one serious accident happens on your property, what is the most that policy can contribute to that one loss?

A good way to read it is to treat per occurrence as the cap on one problem. One slip, one falling tool, one broken panel system, one bodily injury claim tied to that event.

Aggregate means the total available for the policy period

The aggregate limit is the most the policy will pay for covered claims during the policy term, usually a year.

So if the policy shows $2 million aggregate, that is not $2 million available for every claim. It is the total pool available across claims during that policy period. If a company has already had a large claim elsewhere, the amount left for your property may be lower than the original aggregate shown at the start of the term.

That is the part many clients miss. A certificate shows the policy's stated limits. It does not show you how much of that limit may already be eroded by prior claims.

| Policy term | Plain-English meaning |

|---|---|

| Per occurrence | Maximum available for one covered incident |

| Aggregate | Maximum available for all covered incidents during the policy period |

Why this matters more on higher-exposure properties

On a modest residential job, those numbers can feel distant. On a large home, a retail center, or a managed community, they become much more concrete.

High-value glass, custom finishes, metal awnings, stone surfaces, storefront access, tight pedestrian areas, and repeated service visits all raise the financial stakes of one mistake. The question is not just whether a vendor carries insurance. The question is whether the limits fit the property and the type of work being performed.

That is one mark of a professional operation. A company with formal systems, documented safety practices, and the right insurance structure usually understands that a three-story mixed-use property should not be treated like a basic ground-level service call. Clients comparing providers can use that standard when reviewing a professional window cleaning company profile.

If policy wording still feels technical, this plain-English guide on how to read insurance policy can help you review the language with more confidence.

The strongest takeaway is simple. “Insured” is not a complete answer. Limits tell you how much protection may be there when something goes wrong.

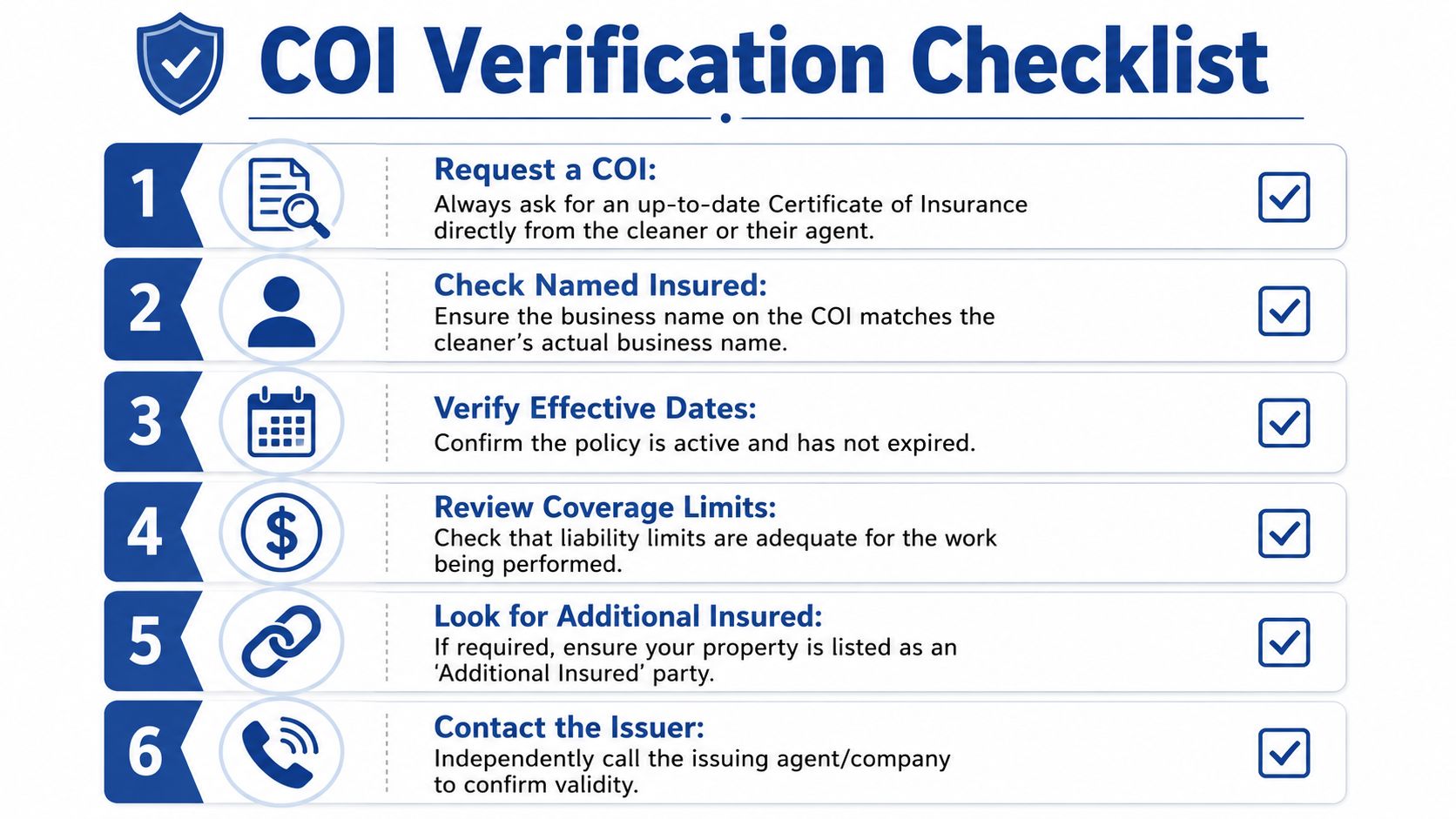

Your Verification Checklist How to Vet a Window Cleaner's COI

A Certificate of Insurance, usually called a COI, is the document clients request to confirm coverage. It's useful, but only if you read it carefully and verify it properly.

The biggest mistake property owners make is treating a COI like a decorative PDF. It isn't. It's a screening tool.

What to request

Start by asking for a current COI before work begins. For recurring service, ask for an updated certificate whenever the policy renews.

If you're reviewing vendors, a company page like this window cleaning company overview can help you confirm whether the business presents itself as a formal operation, but the COI is still the actual document you need to review.

Ask for the COI to come directly from the insurance agent or broker when possible. That reduces the chance of receiving an outdated or altered file.

What to check on the document

Read the COI line by line. You're looking for consistency, clarity, and active coverage.

Business name match

The named insured should match the legal business you are hiring. If the invoice says one thing and the COI says another, ask questions.Effective and expiration dates

Coverage must be active on the date the work is performed. A valid policy last month doesn't help you today.Coverage types shown

For window cleaning, you should expect to see the policies relevant to the scope of work. The certificate should not feel vague or incomplete.Liability limits

Review whether the listed limits fit the property and the work being done. A storefront route is different from a high-rise or luxury residence.Certificate holder details

If you're a property manager, your entity name should appear correctly when requested.Additional insured status

On commercial work, many clients ask to be listed as an additional insured. That can extend protection to the client for claims arising out of the contractor's operations, depending on policy terms and endorsements.

Red flags that deserve a second look

A COI doesn't have to be fraudulent to be inadequate. Watch for signs that the vendor may be underprepared.

- Recent last-minute policy start date: This can suggest the company bought coverage only to satisfy a contract requirement.

- Obvious edits or inconsistent fonts: Any visual irregularity should trigger independent verification.

- Missing policy lines: If a crew has employees and vehicles, but the certificate only shows one line of coverage, ask why.

- Reluctance to provide agent contact information: Professional vendors usually expect verification.

- Generic answers to specific questions: If the company can't explain what coverage it carries, that's a problem.

Ask the insurance question before the first service visit, not after a claim.

The strongest verification step

Call the issuing agent or carrier using independently confirmed contact information. Don't rely only on a phone number typed into the PDF. Confirm that the policy is active and ask whether any requested endorsements, such as additional insured status, have been issued.

For larger commercial accounts, this extra step is worth the few minutes it takes.

Sample email you can use

You don't need insurance jargon to ask the right way. Keep it direct.

Hello, please send a current Certificate of Insurance for your company showing active general liability and any other applicable coverage for the scope of work. Please list our entity as the certificate holder, and if required by contract, please confirm whether additional insured status can be provided. If possible, have the certificate sent directly from your insurance agent.

That one message filters out a surprising number of risky vendors.

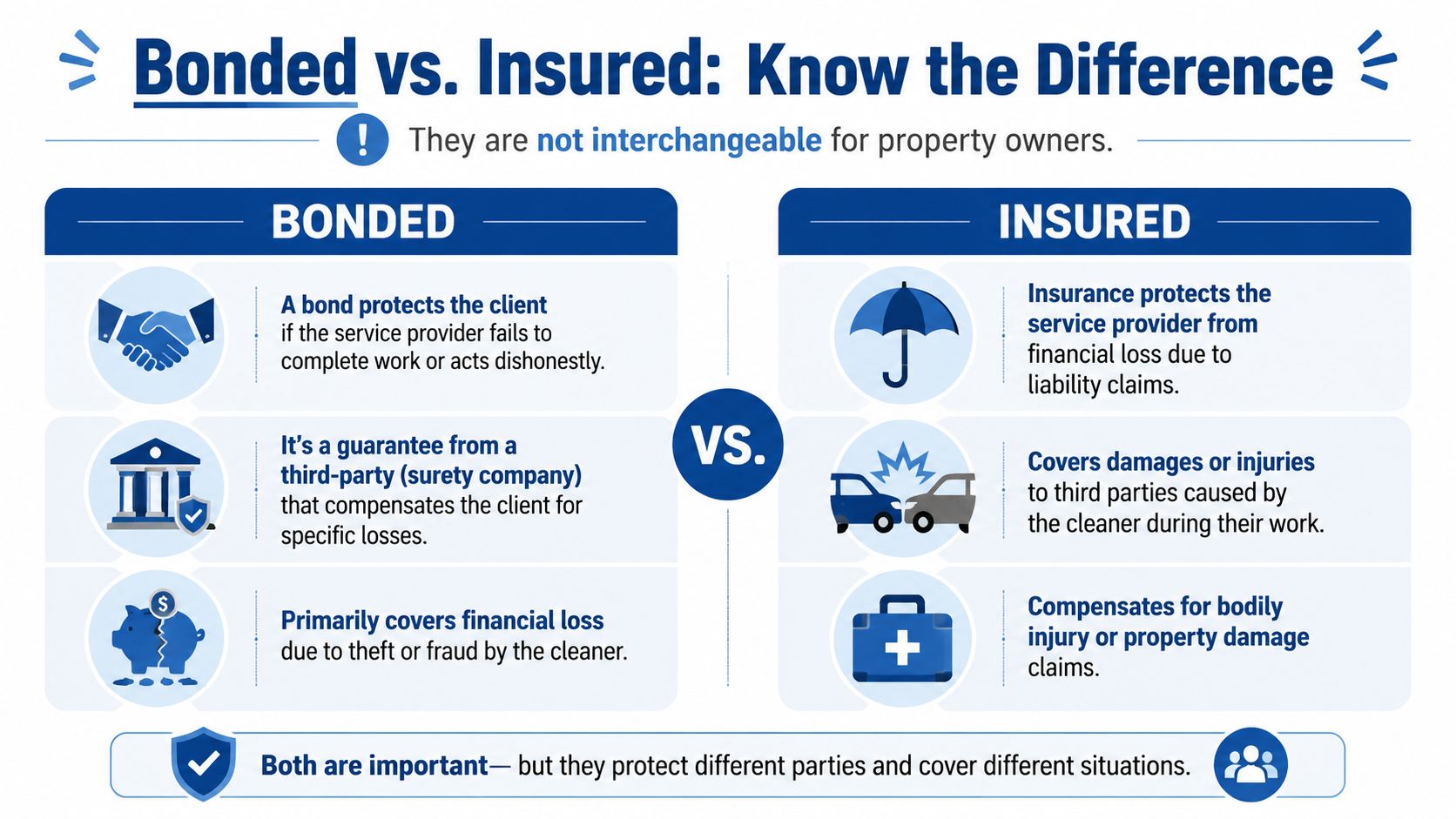

Bonded vs Insured A Critical Distinction for Property Owners

A property owner hires a window cleaning company for a multi-story building. Midway through the job, one technician drops a tool and cracks a skylight. A week later, the owner learns the company was "bonded," but the bond does not pay for accidental property damage. That is the kind of misunderstanding that turns a routine service call into an expensive lesson.

Clients hear "bonded and insured" so often that the two terms start to sound interchangeable. They are not. They address different categories of risk, and knowing the difference helps you sort professional operators from companies using reassuring language without the right protection behind it.

Side-by-side comparison

| Term | What it generally protects against | Why it matters to a client |

|---|---|---|

| Bonded | A specific financial loss defined by the bond, often tied to dishonesty, theft, or failure to meet a contract obligation | Can help with narrow trust-related exposures |

| Insured | Covered claims involving bodily injury, property damage, auto incidents, and other operational losses, depending on the policy | Addresses the accident-related risk created by the work itself |

A bond works more like a limited guarantee than an accident shield. In cleaning trades, that usually means a bond may respond if an employee steals from a client or if a business fails to meet a defined obligation covered by the bond terms. It does not step into the role of general liability, workers' compensation, or commercial auto coverage.

That distinction matters on real jobs. If someone steals a valuable item during service and the bond language applies, the bond may come into play. If a hose floods an interior space, a ladder gouges stone flooring, or a passerby is hurt by falling equipment, you are dealing with insurance claims, not bond claims.

For property owners, the practical rule is simple. Treat "bonded" as an added layer of trust. Treat "insured" as the protection that speaks to accident risk on your property.

This point is easy to miss because vendors sometimes lead with the bond. It sounds reassuring. But if you are reviewing a contractor for exterior or interior window cleaning, the first question should be whether the company carries active insurance that fits the actual work being performed. A bond is narrower by design.

If you want a plain-English explanation to compare against what a vendor tells you, this bonded vs insured comparison lays it out clearly. For broader context on how bonds are tied to specific legal or contractual duties, the overview of Florida small business bond requirements is also useful. It shows why a bond should never be mistaken for broad accident protection.

What Proper Insurance Costs A Look at Phoenix Pricing Factors

A window cleaning proposal can look attractive on paper until something goes wrong on your property. At that point, the cheapest bid often becomes the most expensive choice if the company cut corners on insurance.

Insurance cost is part of the operating reality of a legitimate contractor. A professional window cleaning company has to carry that expense the same way it carries payroll, vehicles, ladders, water-fed poles, and safety training. If you are comparing vendors, that matters. You are not only buying clean glass. You are also deciding how much risk the company is prepared to absorb before that risk reaches you.

According to MoneyGeek's cost analysis for window cleaning insurance, a small window cleaning business averages about $97 per month, or $1,165 per year, for five common coverage types at standard $1 million per occurrence and $2 million aggregate limits. The same analysis shows that pricing can vary widely by state, with lower averages in some markets and much higher averages in others. That range helps explain an important point for Phoenix clients. Insurance pricing is never one-size-fits-all.

Why Phoenix pricing isn't one-size-fits-all

Insurers price risk based on the local market and the shape of the company they are covering. In Phoenix, that can mean a different mix of exposure than a small town route business in another state. A company servicing dense commercial corridors, driving across the Valley every day, and working on larger properties will not be viewed the same way as an owner-operator cleaning a handful of ground-level homes nearby.

Here are some of the factors that commonly affect what a window cleaning company pays:

- Type of work performed: Interior storefront work, residential ladder work, and multi-story commercial service do not create the same exposure.

- Vehicle use: More time on the road and more equipment in transit can increase auto-related risk.

- Employee count: More technicians usually means higher workers' compensation costs.

- Claims history: Prior losses often lead to higher premiums or tighter underwriting.

A helpful way to view this is to compare insurance to the foundation under a building. You do not see most of it during a routine visit, but the size and condition of that foundation affects how safely everything above it operates.

What clients should take from that

An unusually low bid should prompt questions, not assumptions.

Sometimes a company is efficient. Sometimes it has lower overhead for legitimate reasons. But sometimes the price is low because the business is carrying minimal coverage, excluding part of its work from coverage, or operating with gaps that only become visible after an accident.

That is why experienced property managers and careful homeowners do not judge proposals by cleaning price alone. They look at the full operating picture. Is the company staffed properly? Does it use trained employees or casual labor? Does it maintain vehicles and equipment? Is insurance part of the job cost, or missing from it?

If you want a clearer benchmark on the service side before comparing bids, this guide to the average cost of window cleaning in Phoenix can help. Use it alongside insurance verification, not as a substitute for it.

A professional contractor prices for the work and for the risk that comes with the work. That is one of the clearest differences between a company that is built to protect your property and one that hopes nothing goes wrong.

Partnering with a Protected and Professional Service

Clean windows matter. So do curb appeal, natural light, tenant experience, and presentation. But insurance is what turns a window cleaning company from a vendor into a professional contractor you can responsibly allow onto your property.

The strongest clients ask better questions. They ask what coverage is in place, whether limits fit the job, whether the COI is current, and whether additional insured status is available when needed. They understand that “bonded” and “insured” are not interchangeable. They know a polished website doesn't replace verified documentation.

For property managers, facility teams, and homeowners in Phoenix and the surrounding Valley, that mindset reduces surprises before a job starts.

If you're reviewing providers near you, this local window cleaning service directory can help you compare options by service area and property type. The right partner doesn't just deliver clean glass. The right partner arrives prepared, documented, and accountable.

If you're looking for a protected, professional contractor for residential, commercial, or high-rise service in Phoenix, Scottsdale, Paradise Valley, Chandler, Tempe, or Gilbert, contact South Mountain Window Cleaning, LLC. Ask for current insurance documentation, confirm the scope of work, and make sure the company you hire protects your property as carefully as it cleans your glass.